Planned Giving

Having a game plan is key. Helping us plan for the future through assistance from your estate, will or living trust can provide benefits in perpetuity.

What is Planned Giving?

Planned giving allows community members and fans to pursue their intention to contribute a major gift to the Rose Bowl Legacy Foundation, beyond their lifetime. At times, this can offer different tax advantages to the donor. The Legacy Foundation offers several options for planned giving.

A Gift Annuity that Benefits You

In Giving you receive

You can make a generous gift to the Rose Bowl Legacy Foundation, while providing a secure, fixed income for life for yourself, you and a loved one, or another person. You make a gift of cash or stock to the California Community Foundation (CCF), Pasadena Community Foundation (PCF), or another accredited organization and designate the Rose Bowl Legacy Foundation.

In some situations, such as working with the Pasadena Community Foundation, designation of the Rose Bowl Legacy Foundation will allow us to receive an immediate grant. In return, the PCF will make annual payments to you which are guaranteed for life.

Charitable Gift Annuities’

To qualify for a Charitable Gift Annuity you must be 65 years or older and your gift must be a minimum of $10,000. Each annual payment is fixed as of the date of your gift. That means your payments will never change, even if interest rates or the stock market changes. It does not fluctuate. The amount depends upon the age of the person who receives the payments. You will also receive a significant tax deduction in the year that you set up the gift annuity.

PLANNED GIVING

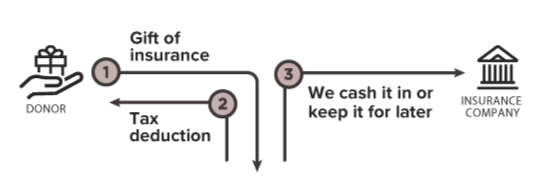

Life Insurance

You can provide now for a future gift to the Legacy Foundation by naming us owner and beneficiary of a life insurance policy. When the policy matures the proceeds are paid to the foundation and we apply them to the program you have designated.

Benefits

- You can make a significant gift from income instead of capital.

- Your gifts offsetting our premium payments are fully deductible.

- You build our future financial strength.

The Details

Donate a policy, take a deduction, deduct future premium payments, if any, and make an extraordinary gift. You’ll also get the proceeds out of your taxable estate.

Is This Gift Right for You?

A gift of life insurance is for you if:

- You are a younger donor who wants to make a significant gift.

- Your estate probably won't have substantial assets to distribute to non-family members.

- You can make a commitment to provide gifts that will offset our premium payments on the policy.

Your financial projections may indicate that you won't accumulate large blocks of capital during your lifetime, or that your family will have control on your estate. You want to make a significant gift to the Rose Bowl Legacy Foundation but wonder if you'll need the resources to do so.

Life insurance uses manageable payments made from income — the premiums — to create a large future gift for the Rose Bowl Legacy Foundation. You can build our long-term financial strength without diminishing your own.

Make the gift by taking out a new policy on your life, naming the Rose Bowl Legacy Foundation as the irrevocable owner as well as beneficiary (this arrangement makes the gift complete in the eyes of the IRS.) We will receive the premium notices, and you will make annual donations to offset our payments. These gifts will, of course, be tax-deductible. There is no deduction for setting up the policy itself.

Besides creating a new life insurance policy, you can also donate an existing policy. This gift will generate an initial tax deduction: the lesser of the policy's fair market value — we can guide you in determining this — or the total of your net premium payments. If premiums are still payable, we will ask you to make tax-deductible contributions offsetting our payment of those premiums. We do reserve the right to keep such a policy in force during your lifetime, or to terminate it sooner for its cash-surrender value.

PLANNED GIVING

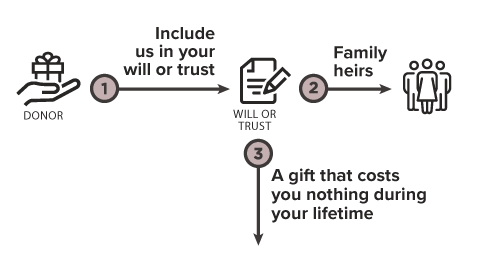

Living Will & Trust

Include a bequest to the Legacy Foundation in your will or trust making it unrestricted or direct it to a specific purpose. Indicate a specific amount, or a percentage of the balance remaining in your estate or trust.

Benefits

- Your assets remain in your control during your lifetime.

- You can modify your bequest to address changing circumstances.

- You can direct your bequest to a particular purpose (be sure to check with us to make sure your gift can be used as intended).

- Under current tax law there is no upper limit on the estate tax deduction for your charitable bequests.

The Details

It just takes a simple designation in your will and will not affect your cash ow during your lifetime. It’s easy to revoke if your situation changes.

Is This Gift Right for You?

A bequest is for you if:

- You want to help ensure the Rose Bowl Stadium’s future viability and strength.

- Long-term planning is more important to you than an immediate income-tax deduction.

- You want the flexibility of a gift commitment that doesn’t affect your current cash flow.

Your bequest to support our mission should be thoughtfully planned. Many good planning techniques are available, and you should choose the type of bequest that best suits your personal objectives.

For example, your bequest can be a stated dollar amount, or you can bequeath specific property to our organization. Some of our friends prefer to bequeath a certain percentage of the remainder of their estate— the amount that remains after paying all debts, costs, and other prior legacies.

Whichever form you prefer, you can direct that your bequest be used for the general support of our work or for a specific purpose you designate. Whatever your objectives, we will be happy to work with you in planning a bequest that will be satisfying, economical and effective in carrying out your wishes in our important mission.

PLANNED GIVING

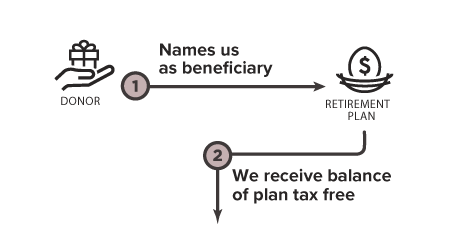

Retirement Plan

Name the Legacy Foundation as a beneficiary of your IRA, 401(K) or other qualified plan and designate us to receive all or a portion of the balance of your plan through your plan administrator.

Benefits

- Avoid the double taxation your retirement savings would incur if you designated your heir(s) as beneficiary(ies).

- Continue to take regular lifetime withdrawals.

- You can revoke us as a beneficiary if your family's needs change.

The Details

Your retirement fund can be taxed up to 80% if passed on to heirs, yet it’s tax-free to charity. Often, between paying taxes and receiving a deduction, using a lifetime withdrawal to make a gift to charity is a “wash” for tax purposes.

Is This Gift Right for You?

A gift from your retirement account is for you if:

- You hold a 401(k), IRA, or other retirement plan.

- You prefer to make a gift to us through your estate plan.

- You want to balance your giving between providing for your family and for us.

- You want to ensure the most efficient distribution of the assets in your estate.

If the largest asset in your estate is your retirement plan, such as a 401(k), IRA, or Keogh, you may be surprised to learn that the IRS will impose income tax on the remaining balance in the account if you designate it to a beneficiary other than your spouse.

This tax is in addition to the estate tax that may be imposed on the account. For estates fully subject to the estate tax, the result can be that up to 60 percent of the value of your retirement plan will be consumed in taxes before your child, relative or friend receives it.